The article was written by Motek Moyen Research Seeking Alpha’s #1 Writer on Long Ideas and #2 in Technology – Senior Analyst at I Know First.

published on: https://iknowfirst.com/intel-stock-forecast-why-intel-can-hit-65-next-year

סיכום:

נמורה אינסטינט ( בית השקעות) יזם לאחרונה דירוג קניה למניית אינטל, מחיר היעד שלו היה 65 דולר. נומורה טוען, שההובלה שלה בתחום הבינה מלאכותית ונהיגה אוטונומית, יכולה להגביר את המכירה השנתית ב 7-9 אחוזים משנת 2020 ועד לשנת 2025. דויד וונג, האנליסט של נמורה אינסטניט עוד הוסיף, שבטווח הארוך זה יכול להגדיל את הרווח למנייה. אני מאמין לתחזית של וונג. וחושב שאינטל תגיע עד סוף השנה ל-65 דולר. כרגע מחיר המניה 56 דולר. והיא מתחת לשווי הגלום ביחס למתחרותיה.

I remain long Intel (INTC) because of its monopoly on data center/server processors. However, I agree with David Wong (a senior equity analyst at Nomura Instinet) that INTC is a buy right now. David Wong is a famous semiconductor industry-centric equity analyst. Wong said INTC deserves a $65 price target. I also rate INTC a buy. This stock already touts a YTD return of 18.22% but I’m highly confident it has more upside potential before 2019 ends.

(Source: Seeking Alpha)

Wong’s PT of $65 for INTC is a good follow up to the $62 PT of Bank of America Merrill Lynch analyst Vivek Arya, and the $64 PT of Morgan Stanley analyst Joseph Moore. I share these analysts’ optimism over INTC. My fearless forecast is that INTC can hit $65 by early 2020.

Why INTC Should Breach $65

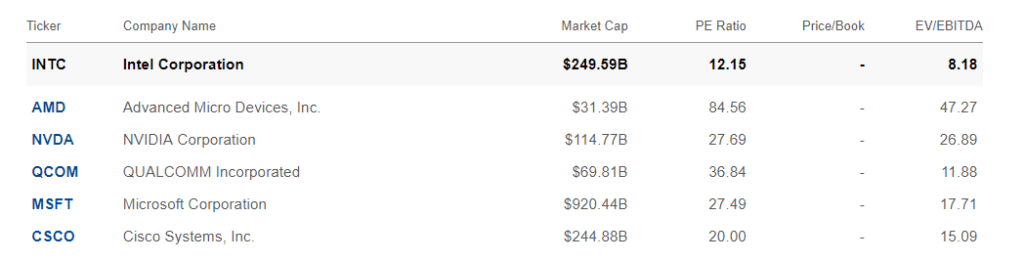

Intel’s stock deserves a $65 price because its 98% market share in server processors is unassailable. INTC still trades below $56. This is pure under-appreciation of Intel’s monopoly on high-margin server and data center processors. This injustice will eventually get corrected once more institutional and hedge fund managers realize that INTC is relatively undervalued compared to its semiconductor peers, Advanced Micro Devices (AMD) and Nvidia (NVDA).

I am long INTC because it is grossly undervalued against AMD and NVDA. Refer to the chart below, INTC’s P/E and EV/EBITDA ratios are notably lower than that of AMD and NVDA’s.

(Source: Seeking Alpha)

The undervaluation of INTC is even more insulting because it’s a solid dividend-payer. Intel makes so much money from its monopoly on server processors (and dominance of PC processors) that it never missed dividend payments since 1997. Note that Intel also consistently raised its annual payments.

The strong revenue/net income performance made INTC a rockstar income investment. This is why INTC attracted 124 ETFs and 2,425 institutional investors (mutual funds, hedge funds, equity speculators).

Intel Is King Of Data Center Processors, AI, and Autonomous Cars

Wong’s perception is that Intel’s industry leadership in autonomous car and Artificial Intelligence semiconductor products can boost its annual sales by 7% to 9% from 2020 to 2025. Going forward, sales of higher-margin self-driving car and AI processors can lead to better long-term EPS (Earnings Per Share) growth performance.

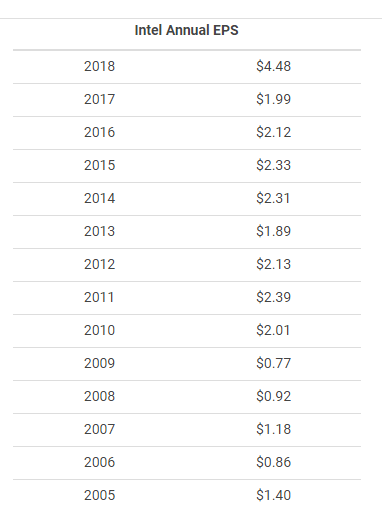

It follows that strong annual revenue growth rate produces better EPS. Please refer to the chart below. Based on the figures below, I predict that Intel’s continuing dominance of the PC/server processor business can help it deliver an EPS CAGR of 10% for the next 10 years. Based on last year’s EPS of $4.48, FY 2019’s EPS could turn out to be $4.93.

(Source: MacroTrends)

Intel wrapping up FY 2019 with an EPS of $4.93 (or $5) coupled with more optimism from 2,000 more institutional investors could drive the stock to $65. My ideal scenario is for the stock market to give INTC a P/E ratio of 13.

EPS of $5 multiplied by 13x, is equal to $65.

The guesstimate above illustrates that the price target of David Wong is really easy to achieve. It only needs more investors to give Intel’s stock a higher valuation.

Final Thoughts

If you like bargain stocks, INTC should be your first choice. It is notably undervalued compared to its semiconductor industry peers. Intel is a super-dominant builder and vendor of PC, server, AI, and self-driving car processors. AMD really has almost zero chance of disrupting Intel’s 98% grip on server/data center x86 processors.

AMD does not have any answer to scalable Xeon processors, Movidius VPUs, Altera FPGAs, Mobileye platform, and Nervana AI processors. All the recent acquisitions of Intel made it the real king of Artificial Intelligence computing and self-driving car ecosystems.

I Know First does not share my super bullish sentiment over INTC. Intel’s stock has neutral 30-day and 90-day algorithmic forecast scores. Its one-year forecast is slightly bullish.

How to interpret this diagram.

Past I Know First Success with Intel Stock Forecast

I Know First has been bullish on INTC’s shares in past forecasts. On January 6, 2019, the I Know First algorithm issued a bullish forecast for Intel. The algorithm successfully forecasted the movement of the INTC’s shares. Until today, INTC’s shares have risen by 17.75% in line with the I Know First algorithm’s forecast. See chart below.